Ultimate Guide to Crypto Staking Taxes in 2026

Here is 2026, and your stakes and rewards are no longer tax-free. Do you know the IRS is cracking down on staking rewards? If you are staking, you are in their crosshairs. To transcend outdated regulations, we are diving into the 2026 changes that will significantly impact your portfolio. This article will help you understand the rules and stay informed. Let's break down the complexity of staking taxes and ensure you’re fully prepared for the tax implications.

Minor Updated Article: January 26, 2026

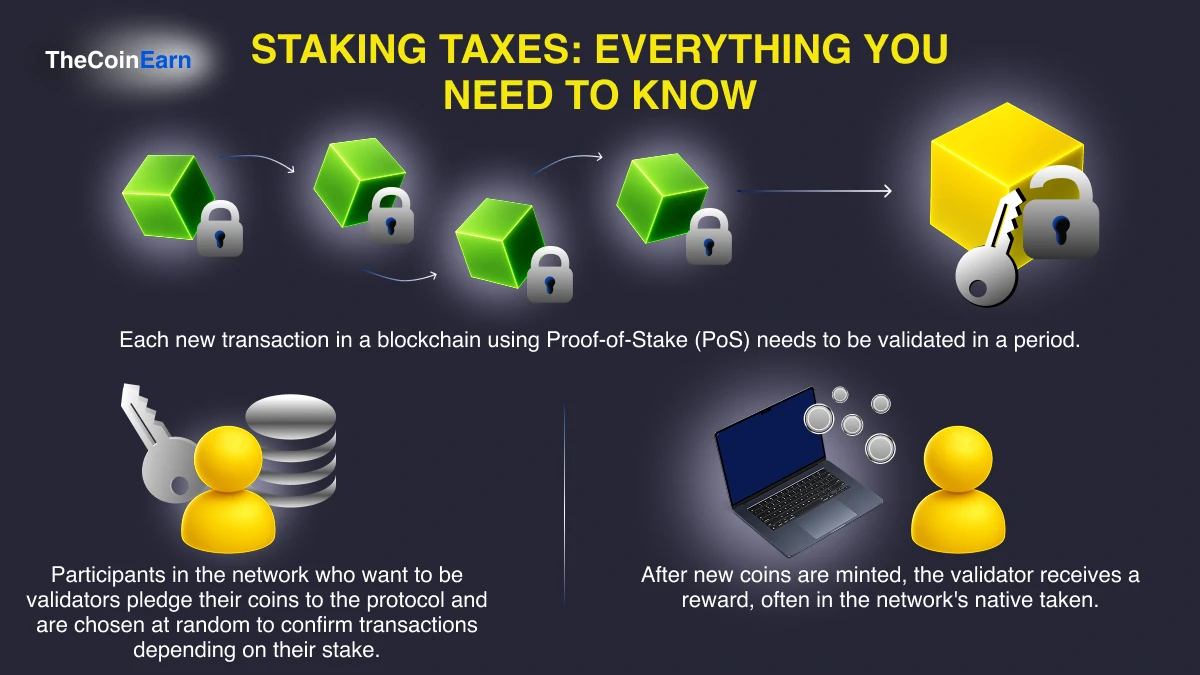

Staking Taxes: Everything You Need to Know

Crypto rewards are generally taxable, including staking earnings, even though they can be a fantastic way to generate passive income. You can stay compliant and steer clear of unforeseen liabilities by being aware of how staking is taxed. This is a brief explanation of staking taxes' operation and significance.

In many jurisdictions, staking is generally considered a taxable event. This is known as “proof-of-stake,” and when you stake cryptocurrencies like Ethereum or Cardano, you use your coins to help validate blocks of transactions on the network. Staking consists of "freezing" your coins, thus allowing them to serve as active actors in network security and integrity.

As you stake, you get chosen randomly to validate blocks, and if you correctly validate these blocks, the more you stake, the higher your chances of being rewarded. You can think of staking as giving your coins a “job”; they are helping to secure the blockchain, and in turn, you get a cut of the network’s revenue.

Understanding Staking Crypto Taxes and Reporting Importance

Overlooking these aspects can lead to considerable risks, as they significantly influence your investment outcomes. While staking rewards can seem appealing, not planning for taxes may result in penalties and compliance challenges.

By understanding staking taxes, you gain a strategic advantage that helps you determine the best times to stake, hold, or sell. A smart tax strategy can unlock value and even lower your tax burden through available benefits. Tax rules vary globally, and what is considered income in one region could be categorized as capital gains in another, depending on local tax regulations.

Stay informed and proactive. Proper tax planning isn’t just about compliance; it’s about maximizing returns and protecting your investments for long-term success.

Crypto Staking Tax Penalties & Consequences Of Non-Reporting

Failing to report staking rewards may have dire consequences because tax authorities have become adept at tracking cryptocurrency transactions. If you ignore these reporting requirements, you will be open to penalties, additional charges on top of those penalties, and possible audits. Consequently, these tend to impose a lot of financial pressure upon you.

Whether you are new to staking or have been doing it for a while, it is a must to keep proper records and get in touch with a tax adviser to ensure you stay clear. Documentation and strong advice are the best methods of ensuring you do not run into trouble and remain compliant.

How Staking Methods Impact Staking Rewards Taxes

There are several staking approaches for you as a beginner to do in the first place:

- Self-staking (Manual): If you prefer to manage things independently, you can deposit coins from your wallet or use staking services. This way, you get 100% of the reward, but it requires time and effort to set up. It’s perfect for those who like to have full control.

- Easy staking (Platform): For a hassle-free experience, stake using big crypto platforms like Binance or Coinbase. Just select the coins you'd like to stake, deposit on the platform, and let the platform do the rest. It's the easiest option for beginners who want to start earning rewards without technical configuration.

- Team staking (Pool): To increase your chances of rewards, consider pooling with others. In this approach, you combine your coins with others in a shared network to enhance the group's staking power as a whole. While rewards are split among members, this is ideal for those with fewer cryptos who want to participate in a significant way.

Here, we can see how the following staking approaches work, each offering unique benefits depending on your goals and resources:

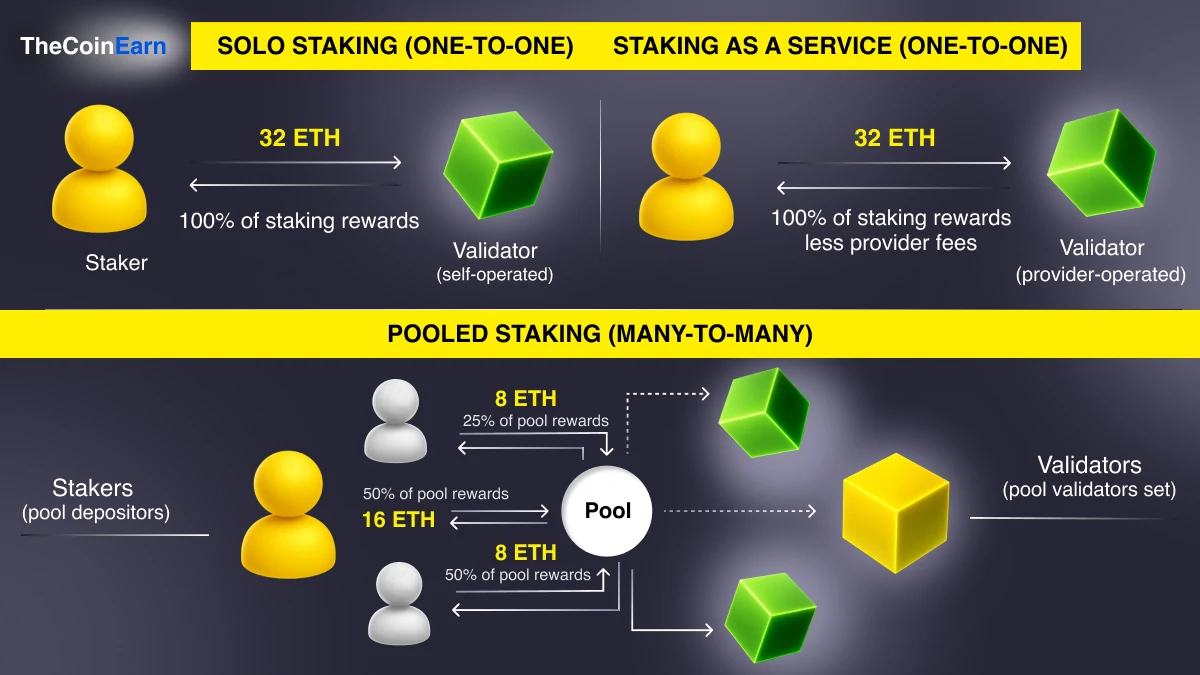

1. Solo Staking (One-to-One)

Solo staking is for those who want full control and maximum rewards. To participate, you’ll need 32 ETH and the technical skills to operate your own self-operated validator. In return, you keep 100% of the staking rewards. This option is ideal for experienced users who prefer complete autonomy and are comfortable managing their own infrastructure.

Tax impact: Rewards are classified as earnings liable for income tax at the moment they are received, with their value determined by the fair market price at the time. Any subsequent sale of these rewards may trigger capital gains tax on the profit earned.

2. Staking as a Service (One-to-One)

If you prefer not to deal with the technical overheads, this option allows you to stake by delegating your part participation in validator operations provided by a third party. You still get 100% of the staking rewards, minus a fee taken by the service provider. The validator is provider-operated, making this a good choice if you're looking to be rewarded without needing to run a validator yourself.

Tax impact: Rewards are similarly taxed as income upon receipt, though the service provider’s fee reduces the net taxable amount. Selling these rewards later may also incur capital gain tax.

3. Pooled Staking (Many-to-Many)

Pooled staking is a collaborative approach where multiple participants combine their resources to meet the 32 ETH requirement. Rewards are distributed based on each participant’s contribution. For example:

8 ETH = 25% of pool rewards

16 ETH = 50% of pool rewards

The pool validator set operates the validator, and participants are referred to as pool depositors. This method is perfect for individuals with smaller amounts of ETH who still want to participate in staking. It’s an accessible way to earn rewards without needing the full 32 ETH upfront.

Tax impact: Your portion of the rewards is taxed as income at the time of distribution, and any future sale could result in capital gains tax.

Across all methods, staking rewards are subject to income tax upon receipt, with potential additional taxes arising from later transactions. To navigate these complexities, meticulous record-keeping and consultation with a tax professional are essential.

Staking offers the ultimate answer to investing your cryptocurrency assets, irrespective of your individual preferences or investment strategy. Select the option best suited to your goal and begin earning money today!

Stake Smart: Managing Crypto Risks

On the surface, staking looks like a simple way to make your crypto work for you, just lock it up and enjoy the rewards. The promise of passive income comes with inherent risks that, if not carefully managed, can swiftly transform gains into losses.

1. Your Private Key is Your Lifeline

If you're staking from your own wallet, your private key is everything. Lose it, and your staked assets vanish, no reset button, no "forgot password" option, just gone.

2. Trusting Third Parties? Think Twice

Using exchanges or staking pools means placing your trust in others. Be aware of the risks:

- Hacks. Cybercriminals often target exchanges, making them vulnerable points.

- Technical Failures. Even the biggest platforms have outages.

- Regulatory Trouble. Governments can shut down services overnight.

3. Market Volatility: Your Silent Enemy

While staking rewards might seem appealing, they can be overshadowed by drastic drops in the coin’s value. A 10% annual yield means little if the asset loses half its value.

4. Staking Wisely: A Proactive Approach

Before diving into staking, take these steps:

- Secure your private key with the utmost care.

- Select platforms that have a strong reputation and a proven track record.

- Get ready for market fluctuations by having a clear strategy.

If staking is done in a smart way, it can be a great way of generating passive income with minimal risks. By keeping yourself informed, diversifying your portfolio, and adopting a long-term perspective, you can negate the downsides of market volatility and get the most out of your staking investments.

How to Report Crypto Rewards on Taxes: Prepare for Your Crypto Tax Bill

Next, we will examine how staking rewards work, and mainly the tax bill that comes with that. It is important to note that taxes might not be as exciting as some of the other issues, but it should be the first concern. That will lead to complications, and it’s much better to have this tax done right. Consequently, we will simplify it to ensure clarity and understanding of how to properly report staking rewards and avoid costly mistakes.

How are Staking Rewards Taxed, and What Qualifies as Income?

Consider staking as a way to earn interest on your cryptocurrency. You earn more crypto as a reward by locking up your coins to help facilitate the operations of the blockchain. How much you earn is based on how much you stake, the network’s rules, and overall activity. Some blockchains provide a fixed reward, while others fluctuate rewards according to usage.

Staking income is usually distributed at regular intervals, daily, weekly, or monthly, based on the network. Usually, the rewards are added to your balance automatically, so your staked balance grows over time.

Regardless of how they're distributed, crypto earnings from staking are subject to taxation at the time they are received, based on their market value at the time.

To illustrate the tax process explained in the accompanying image, consider the following steps.

Step-by-Step Tax Process for Crypto Staking Rewards

1. Earn staking rewards:

- You earn 0.5 ETH from staking. The Ethereum blockchain organization, which encourages decentralized apps and smart contracts, employments the cryptocurrency known as ETH (Ethereum).

- The esteem of 0.5 ETH at the time of receipt is $500.

2. Report as ordinary income:

- The $500 value of the staking rewards must be reported as ordinary income on your tax return.

3. Sell the staking rewards:

- Later, you sell the 0.5 ETH for $750.

4. Calculate capital gains:

- Subtract the original amount ($500) from the amount paid ($750).

- Your $250 is your tax on this sale.

5. Report capital gains:

- The $250 pick-up is subject to a capital pick-up charge, which depends on how long you held the ETH (short-term or long-term).

Understanding how cryptocurrency income is taxed is crucial for any crypto user.

Example:

Consider an individual participating in a proof-of-stake blockchain network, accruing 120 units of the 'NOVA' token as staking remuneration. Upon receipt, the aggregate fair market value of these tokens is $600, constituting ordinary income subject to prevailing income tax regulations.

Subsequently, the individual elects to liquidate the 120 NOVA tokens for a total of $1,000. This transaction yields a capital gain of $400, calculated as the difference between the sale price and the initial valuation. The applicable tax rate for this capital gain, whether short-term or long-term, is contingent upon the holding period of the NOVA tokens before their disposal, wherein short-term gains are subject to ordinary income tax rates and long-term gains may qualify for preferential tax treatment.

Does Staking Crypto Get Taxed, and How to Track Rewards Properly?

Staking rewards are taxable financial gain, similar to regular earnings. When received, record their exact market value at that time. Keep in mind that if you later sell these rewards, you may also owe capital gains tax, which is a tax on the profit made from selling an asset. The amount of tax depends on the profit you make:

- Short-term capital gains (held for less than a year) are taxed at higher rates.

- Long-term capital gains (held for more than a year) generally have lower tax rates.

To ensure compliance with tax regulations and maintain accurate, detailed records of your cryptocurrency activities, it’s absolutely essential to meticulously document every single transaction you engage in, no matter how small or seemingly insignificant. This includes:

- Dates of transactions

Track transaction dates to determine the tax year and holding period, which affects how gains are taxed.

- Amounts received

Record the exact amount of crypto received to accurately report taxable income and calculate tax liability.

- Market value at the time of receipt

Document the market value when rewards are received to ensure accurate income reporting and compliance.

Therefore, maintaining precise records of all staking activities is crucial to navigating the complexities of crypto taxation effectively. Consulting with a qualified tax professional can provide personalized guidance and ensure you remain compliant with the ever-evolving regulations surrounding digital assets.

Staking Crypto Taxes: Key Considerations For Staking Practitioners

Cryptocurrency staking payouts are a great passive income source, but don't qualify you for tax exemption. Most crypto stakers are unaware that receiving staking rewards doesn't imply the rewards are tax-exempt, and tax laws on them also vary depending on your country or jurisdiction. You must report and pay taxes on rewards accordingly to avoid any penalty for non-compliance.

Most jurisdictions treat cryptocurrency rewards as taxable events, and that is the case when it comes to taxation. As soon as these digital assets are placed in your wallet, they are taxable at the fair market value of the day of the deposit. This tax liability is universal, regardless of how you've earned your cryptocurrency, including staking actively or just being rewarded from other mechanisms.

Your exact tax burden will be assessed depending on several factors, which include the current value of your rewards and the tax laws specific to your jurisdiction. Invested in cryptocurrencies, you need to understand how these digital assets would impact your overall tax liabilities.

How is Staking Crypto Taxed Under Different Regulations?

While cryptocurrency staking rewards work much like investment dividends in the traditional financial world, tax authorities are well aware of it, too. When these digital rewards are transferred to your wallet, they should be readily taxed as ordinary income at fair market value upon receipt. This leads to double taxation when you buy assets: you pay income tax at the time of receiving them, and then, if there is a disposition for more than that amount in the future, capital gains taxes are also subject.

The tax implications become very intricate over an extended period of holding these digital assets, particularly when spanning multiple years.

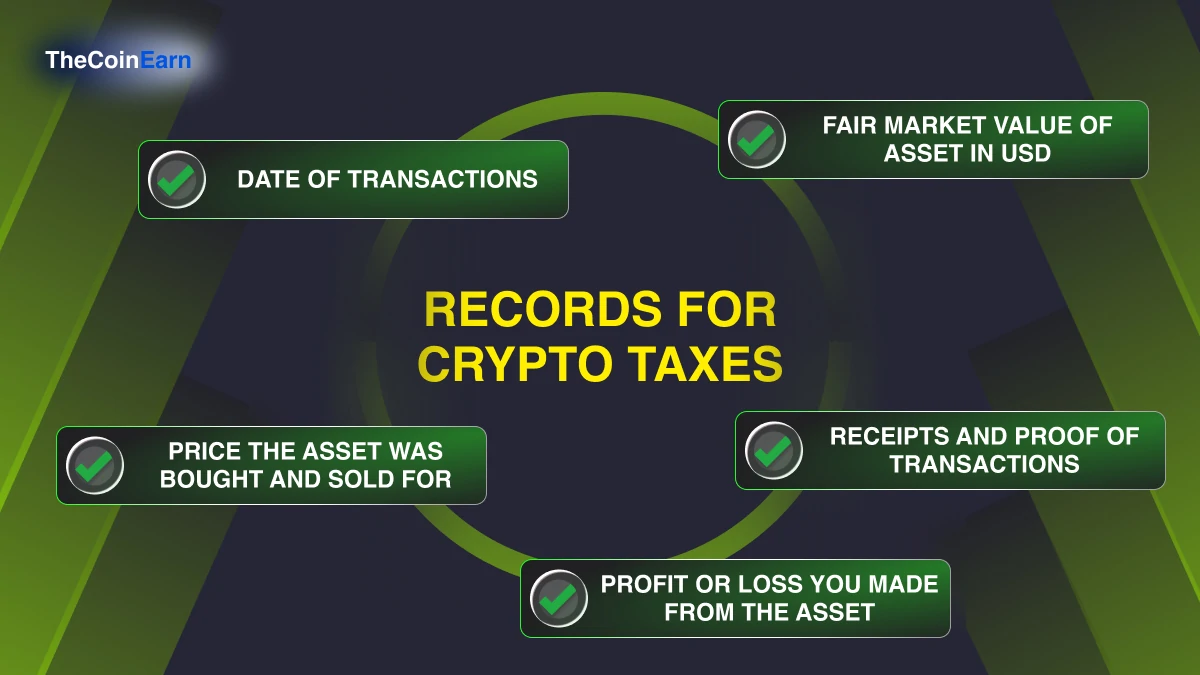

Proper record-keeping is essential for maintaining compliance with cryptocurrency tax regulations. By organizing your crypto activities meticulously, you can accurately report income and capital gains while avoiding potential issues with tax authorities. Here’s what you need to document:

1. Document reward values: Record the precise USD value of each crypto reward at the time of receipt.

2. Track transaction dates: Log the dates of all transactions, including rewards, purchases, sales, and exchanges.

3. Monitor price changes: Keep track of price fluctuations from receipt to sale for accurate capital gains calculations.

4. Save proof of transactions: Store receipts, transaction IDs, and other proof of activity.

5. Record key details: Include purchase-sale prices, profit-loss, and the fair market value of assets in USD.

This organized approach ensures compliance and simplifies cryptocurrency tax reporting.

Where To Report Crypto Staking on Taxes For Compliance?

When it comes to crypto staking rewards, properly reporting them on your taxes is a must to avoid penalties. Whether you're a new crypto staker or a seasoned one, knowing how to work with these rewards and properly report them is imperative. Here's what you need to know:

How to Stay Compliant with Crypto Staking Taxes

Managing staking rewards for tax purposes can be complex, especially as the crypto market fluctuates. Fortunately, specialized tools like Koinly, CoinTracker, and CoinLedger can simplify the process by automating tracking and calculations.

These tools automate tracking rewards, calculating taxes, and generating reports. They integrate with wallets and exchanges to accurately record asset values and compute gains or losses. Not only does it save time, but it also eliminates errors, ensuring compliance with the laws of taxation.

Cryptocurrency tax professionals help with the accurate classification of transactions, optimization of tax liability, and penalty minimization. They understand how to convert complex taxation rules into your specific case, especially foreign transactions or ambiguous situations. They can provide valuable assistance with filing crypto tax returns, understanding tax deductions, and avoiding compliance issues.

Proper tax reporting requires thorough documentation of all transactions: dates, amounts, asset values, and their classification. This helps avoid errors and ensures compliance with tax authority requirements. This includes:

- Income and asset records

- Capital gains summaries

- Transaction history

- Account balances

- Other financial transactions, like gifts and donations

Combining superior organization, specialized software, and professional expertise allows you to master crypto taxation with success. Not only does this guarantee compliance, but it also optimizes returns and reduces risk.

Stake Taxes: A Comparison Between the USA & Germany

Staking tax regulations vary significantly from country to country, so knowing how your country sees crypto is a must. Let’s examine the approaches taken by the United States and Germany as examples. Germany is chosen for this comparison because of its clear and relatively straightforward tax treatment of long-term-held cryptocurrencies; specifically, the exemption from capital gain tax after one year provides a stark contrast to the U.S.’s more complex and consistently taxable approach. This difference in regulatory clarity and tax treatment of long-term holdings makes Germany a valuable case study for illustrating the diverse ways nations handle crypto taxation.

Stake US Taxes & Their Impact On Crypto Trades

In the U.S., the IRS treats cryptocurrency like any other personal asset. Consequently, nearly every trade, sale, or purchase of crypto must be subjected to some form of taxation. Careful recording of events and knowledge of rules will be the key to compliance with legalities. For instance, staking income is taxed from the time it exceeds worth and post valuing at the time you receive it.

When disposing of crypto, the profit is taxed as either short-term or long-term capital gains. It is short-term if sold within the year after buying it up and is subject to taxes of as much as 37%, depending on how much income you earn. It's long-term if it's for more than a year, and taxes are 0-20%, depending on the income again. You will need forms, e.g., Form 8949 for reporting your transactions, Schedule D for your gains and losses, and Schedule 1 for your staking income.

You need particular forms in order to report these activities accurately:

- Form 8949: This is where you report cryptocurrency-related sales, trades, etc. A line-by-line explanation of each transaction to support accurate reporting.

- Schedule D: After filling out Form 8949, you’ll report your capital gains and losses on Schedule D, as this form is filed with your tax returns to provide a summary of the profits (or losses) in cryptocurrencies.

- Schedule 1: Staking rewards are reported as additional income on Schedule 1, which is part of your Form 1040. This ensures that your staking income is properly accounted for and taxed.

In the coming year 2026, Form 1099-DA will be introduced by the IRS to further categorically include the detailed reporting of crypto transactions. This will thereby help the IRS to follow up on the crypto earnings of taxpayers in an effort to ascertain the correctness of tax payments. It is crucial to fill in these forms correctly to avoid penalties or audits.

Are Crypto Staking Rewards Taxable In Germany?

In Germany, the situation is very beneficial when it comes to taxation, especially for long-term investors. Crypto is not considered property but private money, and any profit when selling crypto is completely tax-free if the assets are being held for more than one year. If you sell in the same year, you pay a capital gains tax of around 26.375%, but if the yearly profits you earn are less than €600, you do not have to pay any taxes.

Crypto profit earned by staking, mining, or similar activities is taxed as regular income unless you hold the assets for more than a year, when the assets are tax-free. It's simpler to report crypto transactions to the government than in the USA, where you just report your crypto earnings as part of your tax return, and minor personal gains do not need to be reported. Professional miners and traders are obligated to maintain proper records so their tax statements are correct.

Stake Tax Differences Between Germany & The USA

The taxation of cryptocurrency staking rewards presents a marked divergence between the United States and Germany, requiring individuals to carefully consider their preferred tax implications. The following comparative analysis outlines key distinctions:

| USA | Germany | |

| Crypto Tax Status | No tax exemptions for long-term investors. Crypto is taxed regardless of holding period. | Long-term investors (over 1 year) enjoy tax-free status on crypto. |

| Reporting Requirements | Strict reporting requirements. All crypto transactions must be reported to the IRS. | Less stringent reporting requirements for private investors. |

| Tax burden | High tax burden, especially for active traders. | Low tax burden for long-term investors. |

| Regulatory Security | Increased scrutiny from the IRS, especially with new regulations in 2026–2027. | Lower regulatory pressure. |

| Regulatory Changes | New regulations in 2026–2027 will increase the burden on investors. | Remains a tax-efficient country for crypto investments. |

| Advantages | Clear rules and regulations which may benefit institutional investors. | Tax benefits for long-term investors. |

Final thoughts

Staking is one of the ways to grow your cryptocurrency wealth, but tax obligations should also be considered. This is especially relevant in light of the fact that the rules of crypto taxes are changing so quickly that keeping track of everything is vital.

Staking will be successful with a strategy. That includes details like keeping tabs on staking rewards, staying abreast of the changes in tax regulations, and just adjusting strategies accordingly. Those informed decisions today concerning cryptocurrency staking will earn bolder rewards tomorrow.

FAQ

Are staking rewards taxable?

In many countries, such as the U.S., staking rewards are treated as taxable income in the year you take control of them. You will be required to pay income tax on their fair market value when they are distributed. To ensure compliance, maintain accurate records of the dates, amounts, and values of your rewards.

How to report crypto rewards on charges?

When detailing staking rewards, treat them as standard wages and incorporate their showcase esteem at the time of receipt on Plan 1 (Frame 1040). In case you offer rewards afterward, utilize Frame 8949 and Plan D for capital gains. Keep nitty gritty records of dates, sums, and values. Utilize devices like Koinly or CoinTracker for exactness, and counsel a crypto-savvy to assess proficient in case of uncertainty.

What are the tax implications of holding staking rewards without selling?

Holding staking rewards is not taxable. Keep in mind that in most jurisdictions, the rewards are treated as taxable income at the time you receive them, based on their fair market value. This applies even if you don’t sell or convert them. Always check local tax regulations and maintain accurate records of dates, amounts, and values for reporting purposes.

What happens if I ignore staking taxes?

Tax authorities worldwide are increasingly sophisticated in blockchain analysis and cryptocurrency compliance. Failing to report staking income can result in penalties, interest charges, and potential audits. The financial consequences often significantly exceed the original tax obligation.

Are cryptocurrency tax regulations expected to change in 2026?

In response, tax rules for cryptocurrencies are evolving globally and have been continuously changing. Make sure you remain aware of the shifting regulations relevant to your legal compliance efforts. It involves maintaining a detailed record of every staking transaction, planning the timing of staking for tax benefits, and hiring a crypto tax accountant or consultant.

Will the new 1099-DA reporting cover all staking activities?

The reporting requirements apply to brokers and exchanges, but may not capture all DeFi activities or self-custody staking. Regardless, taxpayers are legally obligated to report all income, even if not captured on a 1099 form.

Is staking a taxable event, and how does that impact your finances?

Staking rewards are subject to tax assessment in most wards, as they are considered assessable wages at the time of receipt. To preserve compliance, speculators ought to keep detailed records of rewards, including their showcase esteem and exchange dates.